The P4H Network and the French National School for Social Security [École nationale supérieure de Sécurité sociale] (EN3S) have been collaborating to document and share knowledge about France’s SHP system and experience in SHP. France’s experience in social health protection (SHP) is one of the richest in the world. The results are noteworthy.

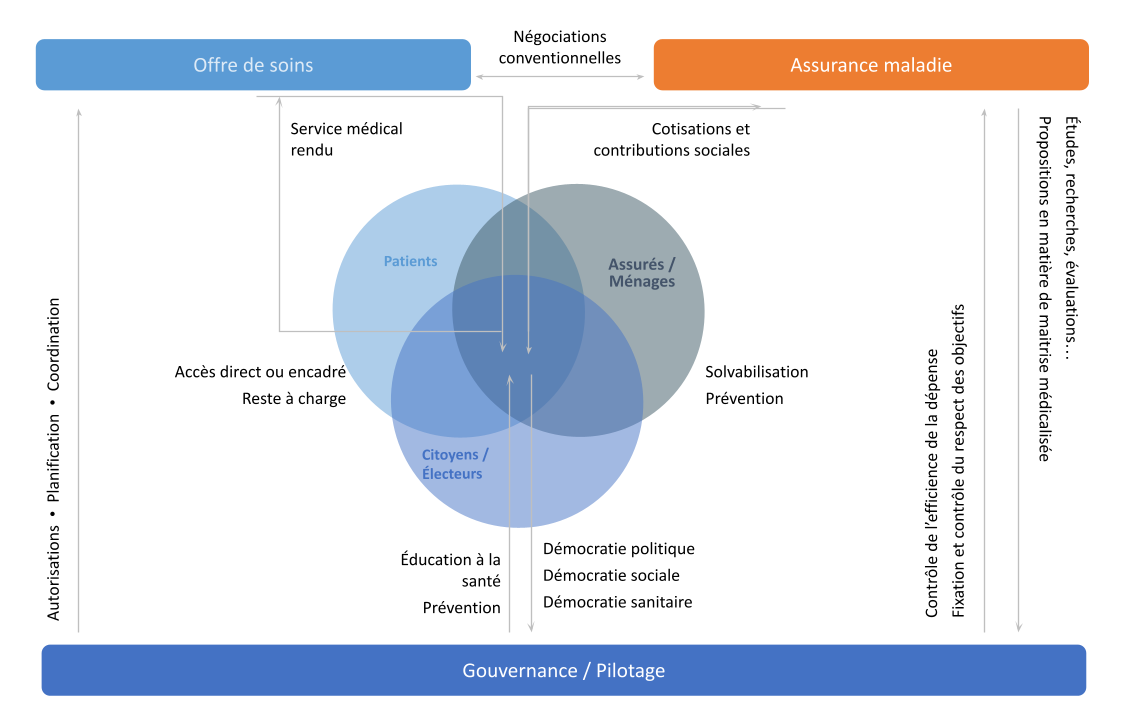

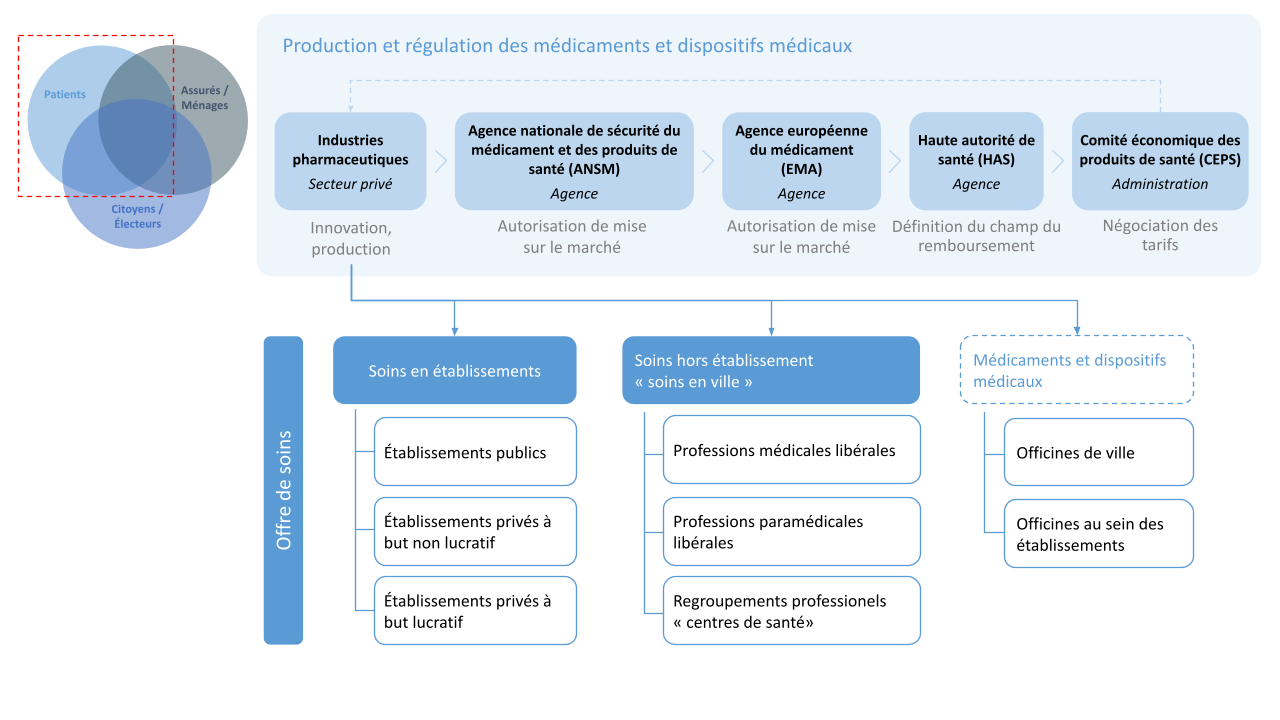

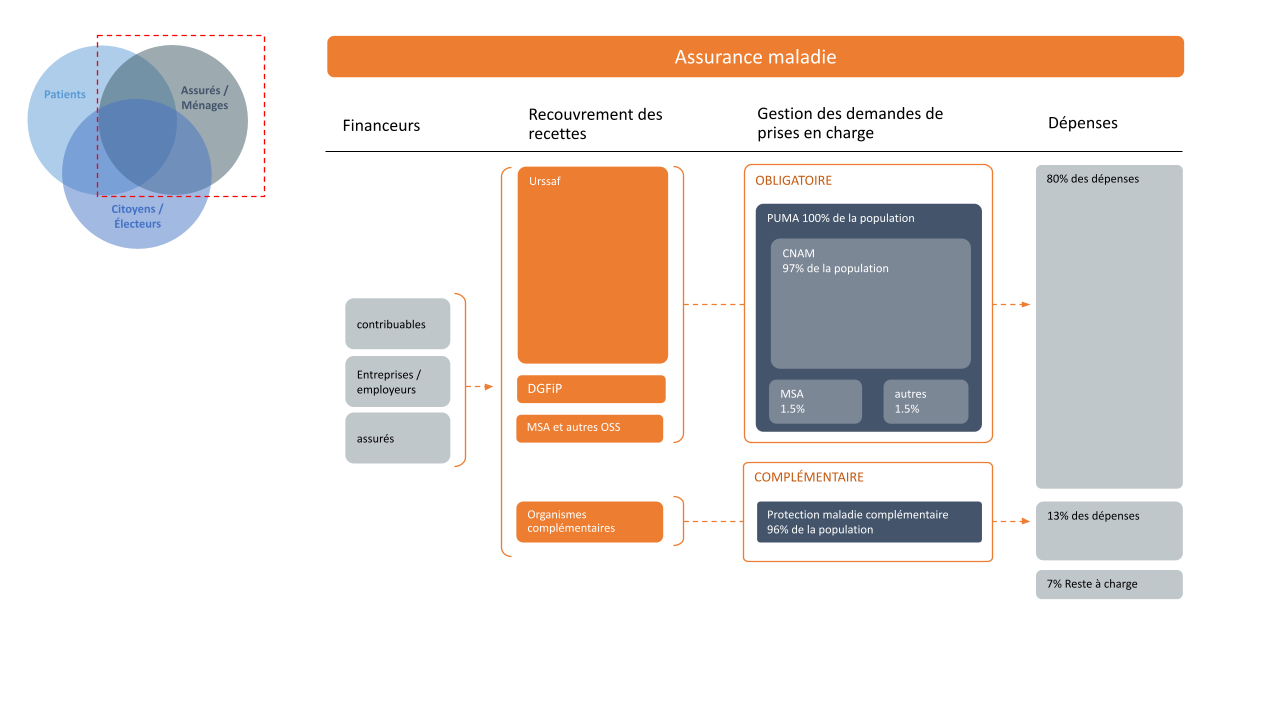

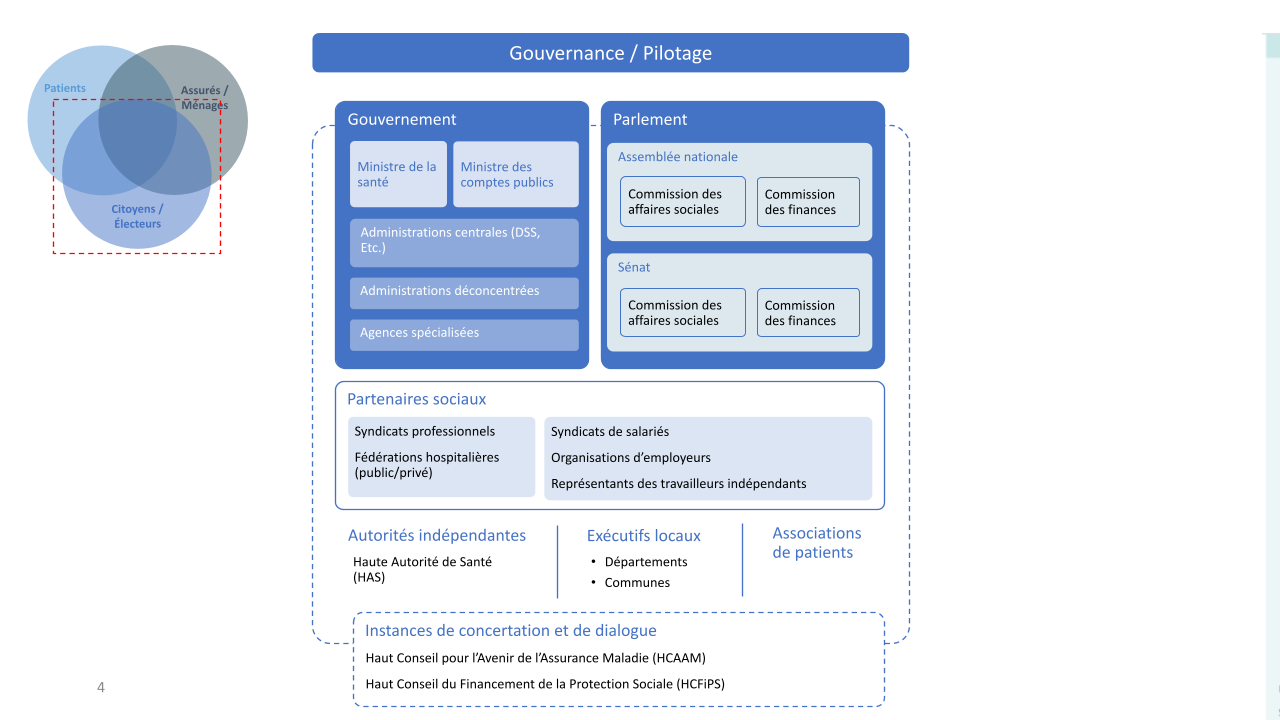

This page invites visitors to view four slides, located at the top of the page. They illustrate the health care ecosystem in France. The slides summarize health care provision, the social health insurance system, and the stewardship of financial risk coverage.

Below the slides, viewers can click on three timelines detailing the history of SHP from the perspective of stakeholders on progress in universal health coverage and changes in health insurance financing.

Below the timelines, readers will find five briefs in French on aspects of SHP in France.

Timely articles from EN3S’s newsletter, Sécu Hebdo, further enrich this page.