By Ms. Tsolmongerel Tsilaajav; Dr. Inke Mathauer and Dr. Valeria de Oliveira Cruz

Thus far, most countries of the South-East Asia Region (SEAR) COVID-19 confirmed cases have occured in clusters. [1] Many governments in the region have relied by and large on public providers to deliver COVID-19 related health services. However, as the situation changes and countries register an even higher number of COVID-19 confirmed cases, governments may have to call for additional support from a wider range of stakeholders, and importantly from private health care providers – where these have a strong presence in the delivery of health services in the region. This is more challenging as the ability to regulate the private health sector has not kept up in most countries. [2] In general, there is considerable variation across countries in the region with regards to private sector health service provision, with countries such as Bhutan, Thailand, Timor-Leste and Sri-Lanka relying largely on public sector providers – while on the other hand, Bangladesh, India and Indonesia have approximately 60%-80% of outpatient visits and 40%-60% of inpatient cases being provided by the private sector. [3] Having effective policies and approaches for private sector engagement (PSE) become thus critical to manage the COVID-19 outbreak in each country.

This blog outlines common policy questions, current country practices as well as policy guidance for purchasing health services from private health care providers in response to the COVID-19 challenges at country level. The purpose is to provide guidance to SEAR countries, share information on experiences within this region and beyond. This is a descriptive account of the early COVID-19 response actions in countries with reflections on existing health financing policy guidance as opposed to any attempt at evaluating actions which will come at a later stage when countries have overcome the emergency situation. The collection of country practices builds on information and feedback from a country survey among focal points in the WHO Country Offices [4] in SEAR to identify experiences in involving and purchasing services from private health care providers. We further enriched the information collected with key WHO recommendations from several recent blogs and documents on health financing [5], budgeting [6] and purchasing [7] for COVID-19 and other sources on strategic purchasing for low and middle-income countries.

2. How are COVID-19 services by the public and private sector providers funded?

Governments are urged to prioritize and fast-track public funds to purchase and provide COVID-19 related health services. Moreover, to ensure effective access to COVID-19 services, WHO recently made recommendations to countries to suspend all types of user fees and cost-sharing for a defined period of time. [5]

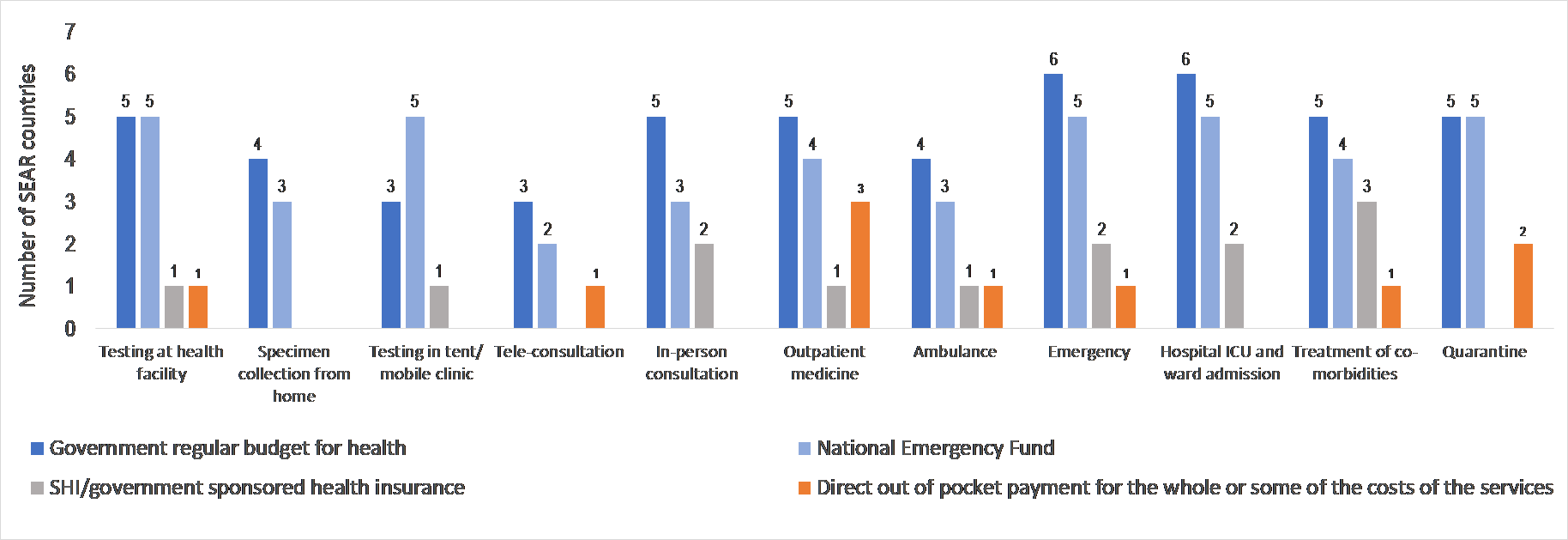

According to respondents, COVID-19 services have been largely funded by government budgets (both regular and for emergency purposes) and also resources from public health insurance programmes such as the Universal Coverage Scheme (UCS) in Thailand and PMJAY in India (Graph 2). In Timor-Leste, an extraordinary transfer was made from the Petroleum Fund (a national wealth fund used for emergency purposes) to the state budget to finance COVID-19 health services.

3. What are conducive purchasing arrangements of health services from private sector providers?

Governments need to clarify which purchasing agency or agencies are to purchase health services from private providers and then need to clarify how to select private providers for the provision of COVID-19 related services. Provider selection can be based on a (minimum) set of standards required where more established regulatory and systematic accreditation is not yet in place.

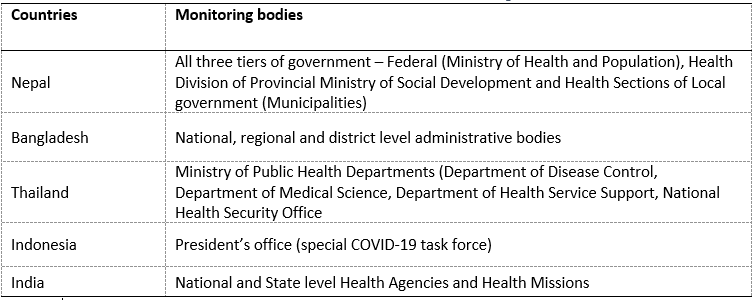

According to respondents, health ministries have been the main coordinators and regulators of the health system related response to COVID-19 in countries in the Region. In several countries, the Ministry of Health (MoH) is also the purchaser of private health care services such as in Nepal, Bangladesh and Timor-Leste. In other countries, public health insurance agencies play the role of purchaser of COVID-19 services from both public and private providers, for example the Thailand’s National Health Security Office (NHSO), Indonesia’s BJPS and the national and state level health authorities in India. For patients that are not enrolled in a health insurance scheme, the Ministry of Health and Family Welfare[1] purchases the required COVID-19 related health services in India, while BJPS in Indonesia is involved in the claims review and verification functions.

With regards to the selection of private providers, there is limited reported information from this survey on whether competitive selection processes or existing accreditation systems were followed when engaging private health care providers for COVID-19 services. Most countries seem to have resorted to more straightforward and faster processes than before where ministries of health and purchasing agencies approved lists of private health facilities for COVID-19 purposes. For example, in Thailand, the Ministry of Public Health issued lists of qualified testing laboratories and approved hospitals for COVID-19 care. In Indonesia, the BJPS certifies private hospitals based on a set of criteria suggested by the Ministry of Health. For example, the capacity in terms of number of ICU beds, ventilators, and health workers, have been used as criteria in these two countries. In other circumstances such as in Nepal, the criterion is more straightforward, namely all designated private facilities licensed as tertiary level health care providers are allowed to manage COVID-19 cases. In India, the state health authorities within PMJAY have the flexibility to loosen the criteria of empanelment factoring in their specific situations.

Governments need to explore whether existing contractual arrangements with the private sector are adequate to scale up private sector involvment, and if not, what kind of adjusments (or simplifications) in contracting arrangements are needed (e.g. with respect to licensing, accreditation, empanelment, etc.) and possible during a state of emergency.

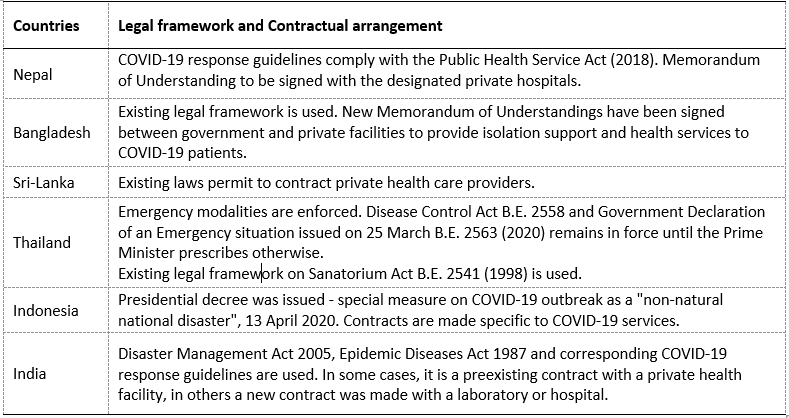

As per the survey responses received, most governments in the region have applied existing legal frameworks to engage private providers in the COVID-19 response (Table 1). A few countries initiated emergency modalities to mobilize additional capacity, e.g. through contractual arrangements with private health care providers during the defined period of the COVID-19 outbreak, like Indonesia and Thailand.

4. Which payment methods are being used and which ones are suited to pay for COVID-19 related services, when provided by the private sector?

The selection of a mix of provider payment methods will depend on the existing payments and claims management system in place and the related set of incentives (including the fast disbursement of funds) towards private providers to enhance increased production of services. While a detailed consideration and flexible adaptation to the country context is needed, the following elements could be explored, for example:

- Fixed amount per test, consultation/ teleconsultation to encourage provision of these services

- Case-based payment for hospital-based COVID-19 care (to be differentiated along severity or use of ventilation, etc. and combined with fee for services (FFS) elements) to ensure continuity and quality of patient care;

- Increase in payment rate to incentivize provision of specific COVID-19 related health services.

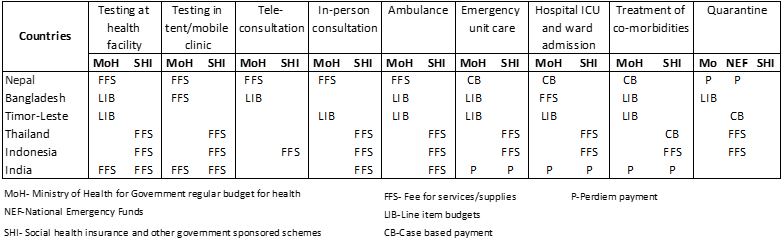

Purchasers and payers in this region apply a mix of payment methods for COVID-19 related services as shown in Table 2. Fee for services (FFS) appears to be the most commonly used payment method, especially for testing, consultation and ambulance services. Hospital care is more complex and hence, various payment methods are used including case-based payment, line item budgets, fee for services and per diem payment.

6. Do existing public financial management (PFM) rules allow for contracting and the purchase of services from the private sector, and what kind of adjustments in PFM rules are needed? How can funds be quickly released to reach frontline providers?

Generally, PFM rules should allow for contracting and buying services from the private sector and allocating funds to the private sector. Recently WHO recommended to countries to explore ways to ensure public resources are made available to the frontlines through timely and effective budget execution processes. [6]

If budgets are formed and disbursed using input-based line items, there may be no mechanism to allow public funds to flow to private providers. Even in countries where contracting with private providers using public funds is allowed, delays in the release of funds also make it difficult for the purchaser to enter into credible contracts with providers. This not only leaves providers with insufficient funds to meet service delivery needs, but it also weakens the purchaser’s ability to implement an effective payment system and establish a trust based contractual agreement. [13]

Countries are exploring various PFM approaches to ensure public resources are made available to frontline providers in a timely and effective manner. It appears that measures such as advance payments or direct budget transfer that aimed at accelerating fund release to providers have been applied to mostly public providers and by the government and the ministries of health. The public insurance schemes tend to use a standard claim-based system or retrospective disbursement arrangements. Nevertheless, the expenditure authorization procedures should be adjusted to accelerate disbursements to reach frontline health care providers in a timely manner while ensuring accountability. [14]

Conclusions

Private providers account for a large share of services provided in the South-East Asia region. As governments harness all available resources and capacities in countries to adequately and efficiently respond to the COVID-19 pandemic, strengthening engagement with the private sector becomes an important policy avenue.

This has been a learning process for all. While the magnitude of challenges differs across countries, each can share approaches and solutions with others who are still looking to address these in the context of this prolonged pandemic. In this process, it is critical that:

- Governments map out the gaps in the public sector and the capacities in the private sector in order to define what services are to be purchased from each of these sectors.

- Funding for the purchase of such services (public health emergency operation response services) should be largely public and direct out of pocket payments by users must be avoided.[5] Therefore, ensuring COVID-19 related services are free of any charges at the point of delivery is vital.

- Strategic purchasing relationships between private providers and governments are established.[7] There is also a need to clarify which agency or agencies are to perform the purchasing functions. In the case of multiple providers serving the same population, the purchasing agencies need to apply a minimum set of criteria when selecting private providers for the provision of COVID-19 related services where more established regulatory and systematic accreditation is not yet in place.

- Governments explore whether existing contractual arrangements with the private sector are adequate to scale up private sector involvement; if not, there is need to define what kind of adjustments (or simplifications) in contracting arrangements are required.

- The selection of provider payment methods will be based on the existing payment and claims management system and more importantly, on the incentive system that the payer or purchaser wants to implement towards private providers.

- Purchasers assess the existing payment rates and whether they set the right incentives for private sector providers. Here, it is important to exercise the need for a balancing act to ensure that financial viability of both provider and purchaser is maintained during this unknown period. Moreover, payment rates need to be adjusted to reflect the relative risks in providing services to COVID-19 patients and the change in the costs structure – which otherwise might compromise the quality and safety of care.

- The public financial management rules allow for a prompt flow of funds while ensuring accountability when disbursing funds to private sector providers.

- Reporting and monitoring mechanisms are to be in place to ensure quality of services through compliance with treatment protocols, patient referral rules, etc.

In moving forward, governments should document, evaluate their responses, and incorporate lessons learned and good practices in strategic purchasing and contracting with private providers as adopted during the COVID-19 crisis to strengthen health systems in the long-term. This will help countries to avoid or reduce risks of future disease outbreaks and other calamities exacerbated due to weak health systems and make them more resilient to future shocks. In doing so, a close focus must be kept on efficiency, quality, and transparency of the health financing systems.

Acknowledgements: We are grateful to the valuable contributions of colleagues in the WHO country offices who contributed information to this blog; we are also grateful to those who reviewed and provided helpful comments, namely (in alphabetical order): Fahdi Dkhimi, Bruno Meessen, Tomas Roubal and Alaka Singh.

[1] WHO, 2020. Coronavirus disease (COVID-19), situation report – 152, 20 June 2020. Available at: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200620-covid-19-sitrep-152.pdf?sfvrsn=83aff8ee_2

[2] Morgan, R and Ensor, T (2016). The regulation of private hospitals in Asia. International Journal of Health Planning and Management, 31 (1). pp. 49-64. ISSN 0749-6753.

[3] Ministry of Health and Family Welfare, Government of India, 2017. Situation analyses- Backdrop to the National Health Policy -2017. Available at: https://main.mohfw.gov.in/sites/default/files/71275472221489753307.pdf

Mahendradhata Y, Trisnantoro L, Listyadewi S, Soewondo P, Marthias T, Harimurti P, Prawira J, et al. The Republic of Indonesia Health System Review. Vol.7 No.1. New Delhi: World Health Organization, Regional Office for South-East Asia, 2017. Available at: http://www.searo.who.int/entity/asia_pacific_observatory/publications/hits/Indonesia_HIT/en/

World Health Organization. Regional Office for the Western Pacific. (2015). Bangladesh health system review. Manila : WHO Regional Office for the Western Pacific., Available at: https://apps.who.int/iris/handle/10665/208214

[4] WHO Country Office Focal Points (health system technical officers) to a differing degree, given the emergency situation in countries, have consulted with counterparts and local experts when providing information to inform this brief. Out of the 11 countries in this region, eight countries responded.

[5] Kutzin J et al. (2020) Priorities for the health financing response to COVID-19, 02 April 2020. Available at: https://p4h.world/en/who-priorities-health-financing-response-covid19

[6] Barroy H, Wang D, Pescetto C, Kutzin J (2020) How to budget for COVID-19 response? A rapid scan of budgetary mechanisms in highly affected countries, 25 March 2020. Available at: https://p4h.world/en/node/8821

[7] Mathauer I et al. (2020) How to Purchase Health Services During a Pandemic? Purchasing Priorities to Support the COVID-19 Response, 28 April 2020. Available at: https://p4h.world/en/who-purchasing-health-services-during-pandemic

[8] WHO, 2020. COVID-19 Essential Supplies Forecasting Tool. Available at: https://www.who.int/publications/m/item/covid-19-essential-supplies-forecasting-tool

[9] Ministry of Health and Family Welfare & World Health Organisation Bangladesh (2018). The Costs of the Bangladesh Essential Health Service Package: Fourth Health Population and Nutrition Sector Programme. Dhaka

[10] Which manages the national health insurance scheme, Jaminan Kesehatan Nasional (JKN).

[11]WHO, 2020. Coronavirus disease (COVID-19), situation report – 152, 20 June 2020. Available at: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200620-covid-19-sitrep-152.pdf?sfvrsn=83aff8ee_2

[12] In India, the largest purchaser is still the Ministry of Health and Family Welfare (MOHFW) through the National Health Mission even though it is rather a passive one.

[13] Cashin C., Bloom D., Sparkes S., Barroy H., Kutzin J., O’Dougherty S. Aligning public financial management and health financing: sustaining progress toward universal health coverage. Geneva: World Health Organization; 2017 (Health Financing Working Paper No. 17.4). Licence: CC BY-NC-SA 3.0 IGO.

[14] Saxena S and Stone M (2020). Preparing Public Financial Management Systems for Emergency Response Challenges. IMF special series on fiscal policies to respond to COVID-19. Available at: https://www.imf.org/en/~/link.aspx?_id=27A8645D20AA4186A005A31874F699D0&_z=z

[15] Ministry of Health and Family Welfare, Government of India. Available at: https://www.mohfw.gov.in/pdf/GuidelinestobefollowedondetectionofsuspectorconfirmedCOVID19case.pdf; https://www.mohfw.gov.in/pdf/FinalGuidanceonMangaementofCovidcasesversion2.pdf

[16] Department of Disease Control, Ministry of Public Health, Thailand. Available at: ddc.moph.go.th/viralpneumonia/eng/guideline_hcw.php

7. What kind of reporting and monitoring mechanisms are needed to ensure service quality by private sector providers?

Effective reporting and monitoring mechanisms need to be in place to ensure quality as well as compliance with treatment protocols and patient referral rules, etc. Monitoring also serves to adapting contractual arrangements over time where needed, e.g. by adjusting incentives for efficiency and quality.

As indicated in the survey responses, one of the first tasks of medical associations and ministries of health with regards to COVID-19 responses has been the updating of operating protocols and guidelines to follow in the clinical management and patient referrals to ensure quality and safety of service delivery. In India for example, the Ministry of Health and Family Welfare (MoHFW) issued several detailed guidelines to clarify referral rules and protocols for all types of providers. [15] Thailand’s Disease Control Department also provided clinical practice guidelines for all health facilities. [16]

Following these guidelines, reporting is mandatory for all types of providers in all countries in the region which require a specific set of data on COVID-19 cases to be reported. In relation to the situation at hand, new mechanisms and platforms are also being put in place to ensure timely and complete reporting of information on COVID-19 related cases. For instance, the Indian National Health Authority established a dedicated and separate platform to collect and analyze the data to monitor changes in the behavior of private providers. In addition, the existing platforms have also been enhanced, for example the Integrated Disease Surveillance Platform in India has been linked to the Integrated Health Information Platform and to the Enhanced Management System/health portal to track information. In contrast, the existing information technology system of the different public health insurance schemes is well established in Thailand and is being applied during the COVID-19 outbreak to capture for example beneficiary registration, provider registration, and claiming processes.

While specific monitoring mechanisms vary, in most countries, not only the purchaser and payer but also the public health emergency regulatory agencies such as Disease Control Departments are more closely involved in the monitoring of COVID-19 service delivery compared to normal times. These agencies can be both at national and sub-national level and in coordination with ministries of health have oversight responsibilities of both public and private facilities (Table 3).

1. What is an appropriate division of labour between public and private providers to deliver COVID-19 and non-COVID-19 health services?

In order to identify potential COVID-19 service providers, countries will have to first assess [8] the gaps in service provision by the public sector to respond to COVID-19. Based on this assessment, there is need to explore available resources and capacities (e.g. Intensive Care Units (ICU) beds, ventilation facilities) of private sector providers and how these could contribute to fill the gaps in service provision; as well as the instruments available on the government side for engaging private providers – for example licensing, contracting, and emergency law empowerment to direct private providers.

The ability of the public health sector to manage a large outbreak is low in many countries of the South-East Asia region. In Bangladesh for instance, government facilities covered on average only 20.4% of the essential health services across the country in 2016. [9] In India, only 50% of hospitals empaneled by Pradhan Mantri Jan Arogya Yojana (PMJAY), a government health insurance scheme to cater to the poor and the vulnerable population, are public.

The government strategy to respond to COVID-19 will need a whole of society approach which will take into account resources and capacity available in all sectors, i.e. both the public and the private sector with respect to the required services, such as testing, ICU beds and ventilators, home care, and case monitoring. In this regard, according to the survey responses, several countries have already scanned the public-sector readiness, private sector capacity and made decisions with regards to their involvement. For instance, the Indonesian Ministry of Health developed stringent guidelines to engage private providers relating to their capacity such as hospitals to have sufficient numbers of medical staff and intensive care facilities. These are applied by the Badan Penyelenggara Jaminan Sosial Kesehatan (BPJS), the national health care and social security agency [10] which certifies them to deliver COVID-19 services. In addition, some governments, like India, Nepal and Thailand, made it mandatory that all designated private hospitals treat COVID-19 cases as per their capacity when and where required.

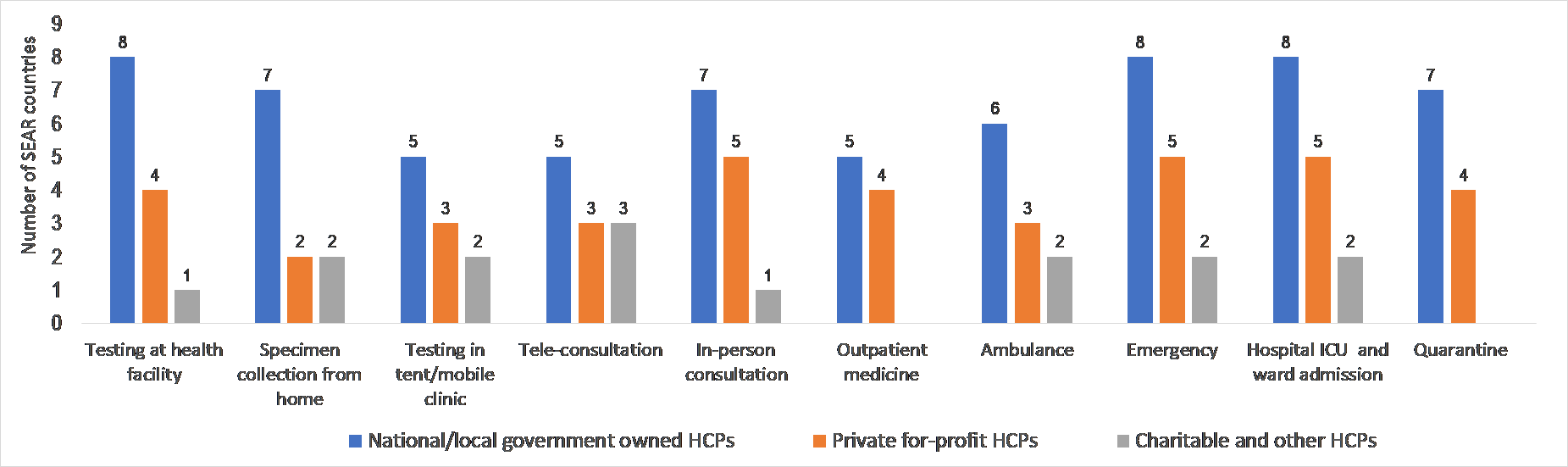

By the mid of June 2020, most countries in the region have not yet experienced community transmission of COVID-19. [11] Nonetheless, in eight countries the private-for-profit providers have already been contributing practically to all COVID-19 health services to a varying degree, such as testing (in health facilities including laboratories), in-person consultations, dispensing of out-patient medicines, emergency room interventions, ICU care, hospital ward admissions and quarantine and self-isolation measures (Graph 1). The contribution by the charitable and other not-for-profit actors across the different services surveyed was found to be less prevalent owing to their size.

In India, the PMJAY and other public insurance schemes pay for enrolled members, whereas the government budgets cover the non-insured patients in public facilities. In Indonesia, a national emergency stimulus package to tackle the COVID-19 outbreak had been earmarked for healthcare spending, since the health insurance legislation excludes healthcare services from BPJS’s funds during emergencies or extraordinary circumstances. The Thai Public Health Ministry declared that all hospitals, public and private, must do their best to treat COVID-19 patients without delay and no hospital is allowed to charge user fees to patients but bill instead public health insurance schemes, retrospectively. Moreover, the service costs of foreign nationals without private insurance coverage have been decided to be paid by the government contingency fund.

Nonetheless, direct out of pocket payments have still been reported as one of the sources of funding for services such as testing at health facilities, purchase of medicines if providers do not have (especially for co-morbidities), and costs of quarantine facilities (Graph 2).

5. How to set tariffs/payment rates for these services purchased from the private sector?

It is critical to assess the existing payment rates and whether they set the right incentives for private sector health facilities to provide the right level and quality of care. Payment rates need to be adjusted to reflect the changes in the service delivery cost structure due to risks associated with providing services to COVID-19 patients. It is also important to exercise a balancing act by ensuring that financial viability of both provider and payer is maintained during these uncertain times.

According to the survey results, private providers in several countries in this region showed some reluctance to provide ICU services for COVID-19 patients at the current payment rates. For example, in Bangladesh private facilities hire consultants and other health workforce at seven to eight times higher rates as health personnel are hesitant to provide COVID-19 services. Therefore, one option is to align or orient the tariffs along the existing payment level, with the possibility to increase it in order to incentivize health care providers. For example, in India, payment rates for COVID-19 related packages were upwardly adjusted factoring in the increased costs. The National Health Security Office (NHSO) in Thailand reimburses private providers at a rate that covers their costs while at the same time still ensuring service quality.

Albeit ad-hoc, there are also some experiences of formal price negotiations to set payment rates, either on a bilateral basis or through group negotiations between purchaser and providers. For example, in Timor-Leste, the private hotels and entities provide quarantine services for COVID-19 suspects and contacts and they are reimbursed at pre-negotiated rates by the government.